Foreclosure happens when a homeowner cannot make timely mortgage payments and lacks the means to catch up on missed payments. Since a mortgage is a binding contract between you and your lender, defaulting on the loan allows the lender to auction your property to recover outstanding debts, leaving you without a home and with damaged credit.

Nobody wants to receive foreclosure notice, yet in a nationwide study, nearly 1 million Americans feared losing their homes (U.S. Census Bureau Household Pulse Survey, fielded from July 27 to Aug. 8, 2022). Foreclosure can result from various circumstances, including:

- Employment termination and income reduction

- Divorce or loss of spouse or partner

- Accumulating debt, including medical and credit card bills

- Relocating without successfully selling the home

- Natural disasters

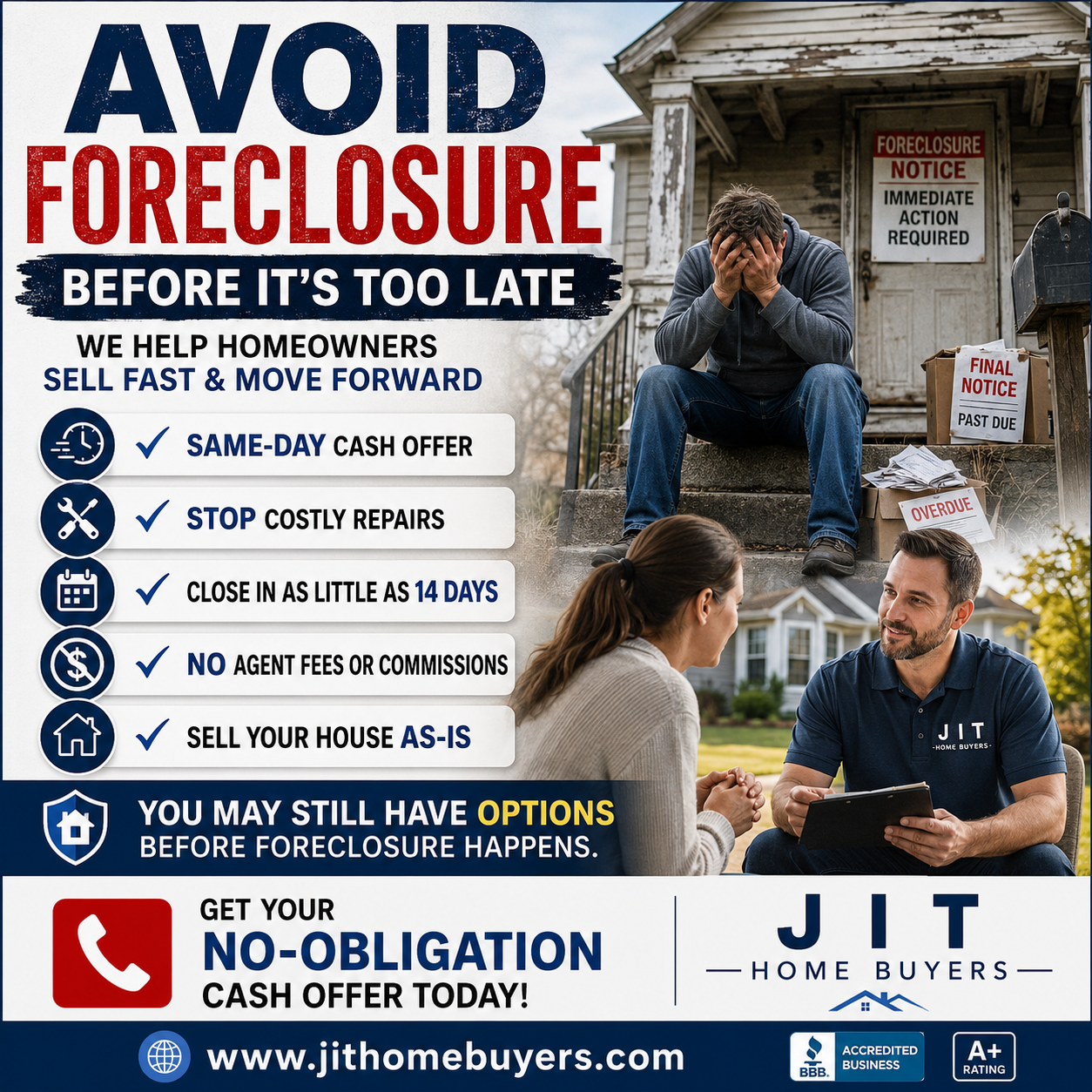

JiT Home Buyers is a local business operating throughout CA that has established their reputation by purchasing distressed houses and properties in the region for cash. They offer competitive cash offers without the complications of working with real estate agents, title companies, traditional bank financing, and more!

What is Foreclosure?

Imagine you or your spouse recently became unemployed. You still face the same financial obligations but unfortunately lack the income to cover your expenses, including your mortgage payment. What’s your next step? Even after securing new employment, the debt accumulated during unemployment might be too substantial to manage reasonably. When this situation occurs, the bank initiates foreclosure proceedings.

How Long Do You Have To Vacate Your House After Foreclosure?

The foreclosure steps in most states include missed payments, public notice, foreclosure, auction, and eviction, but the timeline for each phase varies by state. You could have anywhere from 120 days to nine months before the bank can foreclose using either judicial or non-judicial foreclosure. Throughout this period, your lender will contact you via phone, mail, and email to inform you about the proceedings.

The Different Types of Foreclosure

There are two distinct types of foreclosure you might face: nonjudicial foreclosure or judicial foreclosure.

What Is Non-Judicial Foreclosure?

A non-judicial foreclosure is the quickest and most cost-effective method for a lender to foreclose on your CA property. It doesn’t require taking you, the homeowner, to court and can be executed according to state statutes. In non-judicial foreclosure cases, your lender repossesses your home to sell it and recover owed debt using what’s called a “power-of-sale” clause in the deed of trust. Not every state permits this option, but when available, lenders typically choose it to avoid court expenses.

What Is Judicial Foreclosure?

In states requiring judicial foreclosure, your lender must file a lawsuit requesting the court to issue an order authorizing the sale of the home. The lender must provide you with this notification. Whether you agree or not, you must respond to the letter or the lender will automatically win the case and receive permission to put your home up for foreclosure sale. When the house sells, you remain responsible for paying the difference between what you still owe on the mortgage and the amount the house sold for.

Auctions differ from regular home sales and typically don’t achieve market value prices. This means that even if your house is in excellent condition and worth significantly more than your remaining mortgage balance, you may still owe tens of thousands (if not hundreds of thousands) of dollars for a house you no longer own! This is called a deficiency judgment. It’s an expensive and lengthy process for lenders to recoup their debt, which is why most prefer non-judicial foreclosure.

Get an offer today, sell in a matter of days.

Get An Offer Today, Sell In A Matter Of Days

How to Sell Your House Before Foreclosure in CA

Let’s examine several ways you can sell your house, depending on your timeline and circumstances:

Hire A Real Estate Agent

The first option most Americans consider when selling a house or property is contacting a local real estate agent. But there are advantages and disadvantages to this choice when facing a difficult situation like foreclosure. While a skilled real estate agent can list your property on the MLS and help prepare it for open houses and daily showings, they perform this work knowing that a substantial portion of your sale proceeds will go to them as commission. When you’re already struggling with mounting debt and need every dollar to repay your lender, a commission of 3% to 6% of your final sale price may be too significant an amount to surrender.

Additionally, there’s the uncertainty of not knowing when your house will actually close. Realtors may make promises, but ultimately you’ll still need to find the right buyer and wait 30+ days for a traditional closing. For homeowners facing auction and eviction, even waiting one month might be too long.

Short Sale

If you owe more on your house than its current value, your realtor may require what’s called a short sale. A short sale becomes necessary when you owe more on your house than the property is currently worth. For example: if you owe $200,000 on your house but in today’s market it’s only worth $150,000, you must navigate a short sale. Though it may appear to be a viable option, it won’t be quick or simple.

To begin, you’ll first need your lender’s approval. To qualify for a short sale, you must demonstrate financial hardship using documentation such as W-2s, medical bills, etc. For situations like income loss, the lender will require proof that the income loss is long-term and unlikely to improve in your favor. If the lender approves the short sale, you’ll need to find a real estate agent and attorney specializing in short sales, and they’ll still charge you the same fees as they would for a traditional home sale.

If your foreclosure hasn’t progressed too far and you’ve maintained communication with your lender, they’ll likely approve the short sale. This allows them to avoid the time and expense of foreclosing on your property while still recovering some losses from missed mortgage payments. However, for the average American homeowner, the short sale will impact them for the next 5 to 7 years.

You may have sold the house and paid off some debt, but the short sale can damage your credit similarly to declaring bankruptcy. Credit bureaus include the mortgage delinquency and short sale in their records, making it nearly impossible for former homeowners to obtain credit cards, buy cars, or move into new houses or properties for the same duration as a bankruptcy.

Sell Your House AS-IS to A Cash Buyer

If you’re operating under strict time constraints to sell your house before foreclosure advances to auction and eviction, you have options! You can attempt to sell your property through a real estate agent, work with your lender to complete a short sale, or – most advantageously – turn to a trusted and reliable cash investor to help with your situation.

Some of the advantages of selling to a direct cash investor include:

- A swift and stress-free closing process.

- Avoid paying any commissions or fees.

- You won’t need to worry about marketing your house and waiting for a buyer.

- No need to clean up or complete any repairs!

When you sell your home as-is to a direct cash buyer, you can not only avoid losing your home to auction, but you may also be able to sell the property for enough money to eliminate your financial debt. Moving forward with your life without the burden of monthly mortgage payments and debt weighing you down is one of the greatest gifts you can give yourself!

Can You Stop Foreclosure Once it Starts?

Pay Off Your Loan & Fees

You’ve found yourself in a challenging situation. Your debt is mounting while your finances remain stagnant. It’s time to take decisive action and explore ways to reduce your debt quickly. Do you have any assets you can liquidate? Perhaps you have friends or family who can provide financial assistance or offer you a loan until you regain stability. If you’re committed to paying down your debt and stopping foreclosure, you may need a financial professional to help restructure your budget. Use one of these strategies or combine them all to help tackle that debt avalanche and return to living a stress-free life.

Declare Bankruptcy

As a final option, bankruptcy may help you halt foreclosure of your home, but it comes with significant consequences. The bankruptcy process is complicated and requires a lawyer specializing in bankruptcy law. If the court approves your petition, you’ll enter a government-approved credit counseling program and the bankruptcy will appear on your credit report for 7 years. Bankruptcy affects every aspect of your life, including when you attempt to purchase a vehicle, apply for credit cards or bank accounts, and can disqualify you from future rental applications.

The Homeowner Affordability and Stability Plan (HASP)

If your debt exceeds your income, you may qualify for the Homeowner Affordability & Stability Plan (HASP). HASP is a loan modification program designed for borrowers at risk of foreclosure due to insufficient income. This government program was created to help homeowners in the United States restructure their monthly payments to accommodate a limited budget. Apply for the program here to see if you qualify.

Sell Your House Fast to a Cash Buyer

Are you ready to sell your house but lack the time to wait 30+ days for a traditional closing? Does a short sale seem like a quick way to destroy your credit? Prefer to pay off all your debt at once and get the bank off your back immediately? A direct home buyer and cash investor might be precisely the solution you’ve been seeking! When you work with a trusted and reliable investor with an excellent reputation in your area, you’ll find a helpful company with cash ready to purchase your home as-is. With a cash buyer, you can bypass the lengthy process of foreclosure, eviction, and auction within days while protecting your credit!

You may not receive full market value for your house or property when selling to a trusted cash investor, but the speed of a fast closing and the absence of fees, required inspections, and commissions often balance this out at closing. Best of all, because an investor can close quickly, you can often close before the bank auctions off your property! This means you can sell the property for an amount that benefits you versus the pennies-on-the-dollar price the bank will often try to sell your house for just to remove it from their books.

We Buy Houses in Foreclosure & Pre-foreclosure–

Get Your Offer Today!

Does the idea of finally walking away from a property without the storm cloud of foreclosure hanging over your head appeal to you? Contact a real professional at JiT Home Buyers to learn more and get a fair cash offer for your property today.